The stock market offers an incredible path to build long-term wealth, but it’s easy to underestimate how simple missteps can chip away at your progress—or outright undo years of hard work. When I first started investing, I was surprised by just how many pitfalls there were, and I quickly learned (sometimes the hard way) that even tiny mistakes can have massive consequences over time. In this article, I’ll walk you through the most common ways stock market mistakes cost investors money, highlight real-world stories, and share straightforward strategies to help you avoid these traps. Whether you’re new to stocks or have years under your belt, I promise you: understanding these errors—and what to do instead—can make a dramatic difference in your outcomes and peace of mind.

Quick Summary

- Not researching companies and over-relying on tips is one of the biggest sources of losses.

- Letting emotions dictate trades, such as panic selling or chasing hype, leads to costly decisions.

- Trying to time the market almost always results in missing major rebounds or buying high, selling low.

- Poor diversification and concentrating on one sector, stock, or region can amplify downturn losses.

- Ignoring fees, hidden costs, and tax inefficiencies slowly but surely erode returns.

- Investing without a long-term plan results in scattered, unproductive decisions.

- Overconfidence and excessive trading are consistently linked to underperformance.

- Failing to adjust your portfolio as circumstances change can leave you out of sync with your goals.

- Following the herd or crowd trends, especially via social media, increases risk and volatility.

- Assuming fast, easy, or high returns is realistic for everyone leads to risky bets and disappointment.

Introduction to the Stock Market and Investor Errors

The stock market, at its core, is a place where individuals and institutions buy and sell ownership stakes in companies. These exchanges allow businesses to raise money and investors to participate in the growth and profitability of global enterprises. But the accessibility and excitement of markets conceal traps: emotions, hidden fees, and information overload can all conspire against even the most well-intentioned investor.

My goal in this article is to demystify why stock market mistakes cost investors money—often far more than they realize—and to arm you with knowledge and proven techniques. Prevention is more powerful than recovery; as I learned through my own missteps, it’s easier to sidestep big blunders than to make up for them later. Let’s dig into the 10 most common—and costly—investor missteps, combining research, expert advice, and real-world lessons to help you invest smarter.

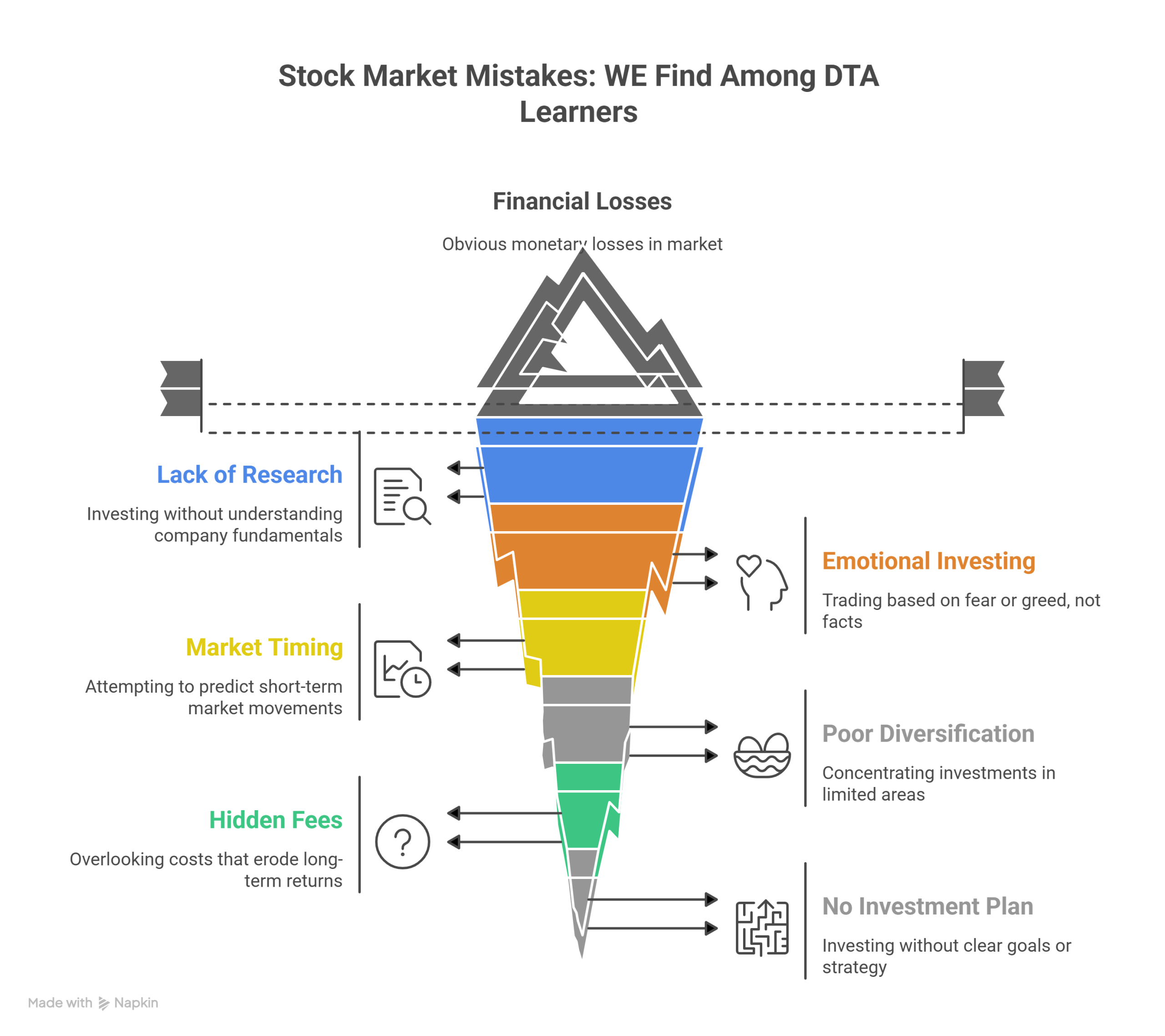

1. Lack of Research

Failing to research investments is arguably the root of most losses in the market. Many investors unwittingly put their money into stocks they barely understand, relying on hearsay, media hype, or tips from friends. A sobering post on the ValuePickr forum summed this up: “Doing less research by myself than to depend on the market gurus” was their most expensive mistake (ValuePickr: Raihan).

Common pitfalls: Blindly following headlines, social media trends, or influencer recommendations. Overlooking fundamentals like company debt, cash flow, and competitive position leads to vulnerability when markets turn.

Solution: Before buying a stock, review its annual reports, listen to earnings calls, and compare its valuation to peers. Check the industry outlook and evaluate management’s credibility. As Warren Buffett famously advised, “Never invest in a business you cannot understand.” Doing your due diligence beats any hot tip.

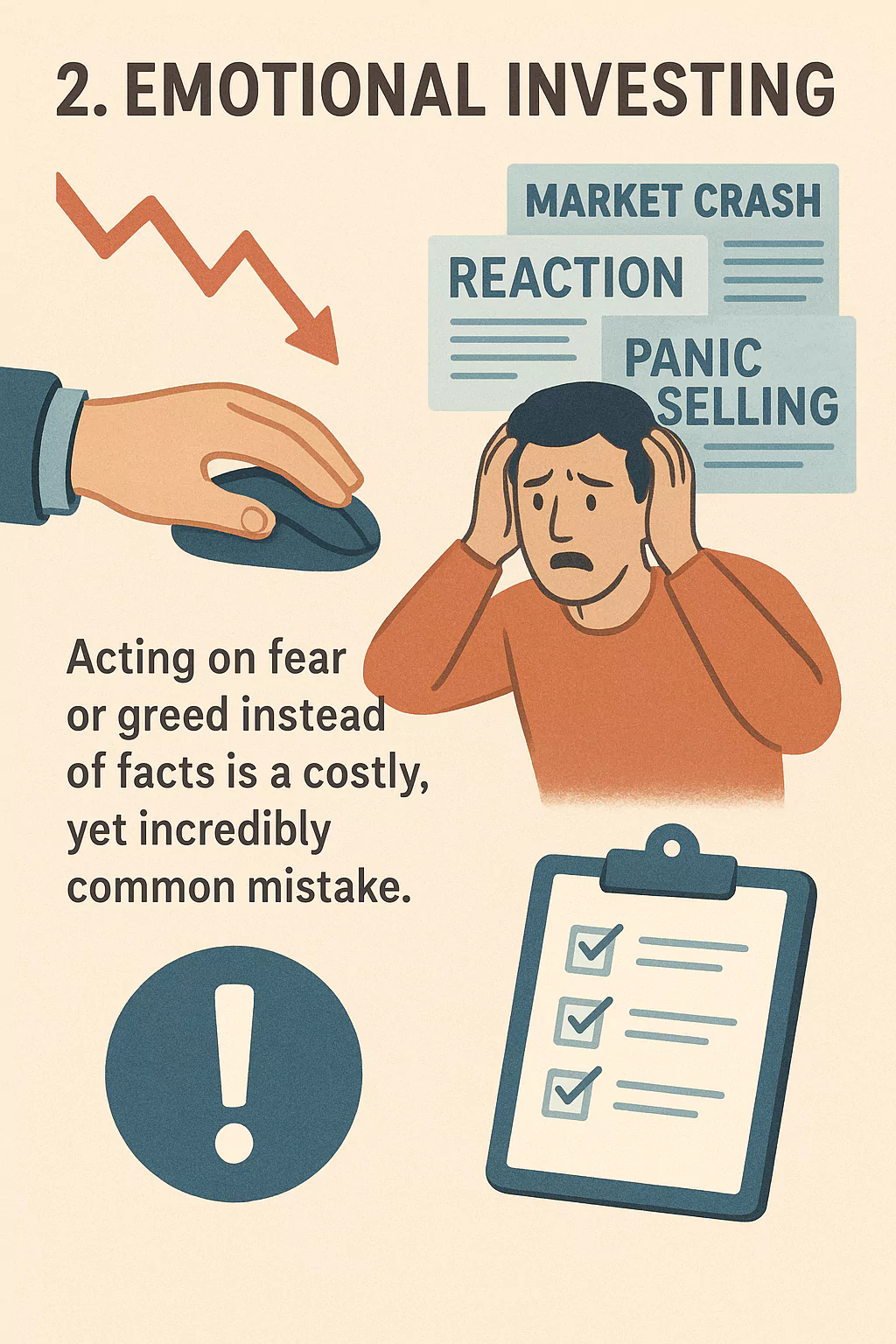

2. Emotional Investing

Acting on fear or greed instead of facts is a costly, yet incredibly common mistake. Investor panic in the face of headlines can easily morph a temporary market dip into a realized loss. During the COVID crash, for example, those who sold during the panic missed out on one of the fastest recoveries in history. In the Bogleheads forum, a user confessed: “I went to cash in early 2020…ouch.” That single word captured the pain of missing out on the rapid rebound (Bogleheads: user John_Bogle).

Common pitfalls: Panic selling during downturns, greedy buying during bubbles, and chasing “fear of missing out” (FOMO) trends.

Solution: Set clear, long-term goals and stick to them, regardless of day-to-day market noise. Use written investment policies or automated investing tools to take emotion out of your decisions. I learned to pause before clicking “sell” or “buy”—giving myself a 24-hour rule to re-check the rational reasons for any move.

3. Timing the Market

The allure of “buy low, sell high” is nearly universal, but trying to time the market is a recipe for underperformance. Multiple studies, including a detailed one from Charles Schwab, show that even the worst market timers who still stay invested beat those who sit out waiting for the perfect pitch (the perils of market timing).

Common pitfalls: Selling after declines out of fear, buying near peaks out of exuberance, and remaining in cash too long “waiting” for an entry point. For instance, a Redditor shared, “I kept waiting for a pullback; meanwhile the market just kept climbing.”

Solution: Implement dollar cost averaging. Stick to a consistent, long-term investment strategy and accept that nobody can consistently predict short-term market moves—even the pros. The best days often come right after the worst, and missing them means missing out on compounding.

4. Lack of Diversification

Putting all your eggs in one basket is a risk few can afford. Concentration in a single stock, sector, or even country can magnify losses. For example, employees overloaded on company stock (think Enron or Lehman Brothers) saw both jobs and savings wiped out (learn more about diversification).

Common pitfalls: Loading up on “winners,” home country bias, and underappreciating cross-sector or currency risks. One ValuePickr user admitted, “I focused on earning big money in small time…big mistake!” (ValuePickr: Vij).

Solution: Spread investments across various asset classes, regions, and industries. Even simple index funds can offer better risk-adjusted returns than concentrated bets. Use automatic portfolio rebalancing to keep diversification intact.

5. Ignoring Fees and Costs

Fees might seem insignificant—but over years, they quietly drain a portfolio. The expert Jack Bogle calculated that just a 1% annual fee can erode up to $100,000 on a $500,000 portfolio over two decades (Vanguard research).

Common pitfalls: Overlooking fund expense ratios, front/back-end loads, frequent trading costs, and tax inefficiencies. As White Coat Investor readers lamented, “Bought a fund with both front and back end loads…learned my lesson the hard way.”

Solution: Choose low-cost index funds or ETFs, double-check for hidden fees, and avoid unnecessary fund churn. Platforms now openly disclose expense ratios and transaction costs—compare before committing funds.

6. Not Having an Investment Plan

“Winging it” rarely pays off in the stock market. Without a roadmap, it’s easy to jump from trend to trend or panic in volatility. I once invested without well-defined goals, and my portfolio reflected the chaos—no clear direction, too much overlap, and random risks.

Common pitfalls: Investing without identifying timelines, risk tolerance, or cashflow needs. Buying and selling based on headlines, not personal strategy.

Solution: Craft a simple written plan: set long-term objectives, determine comfortable risk levels, and clarify your reasons for each investment. Automated contributions (like auto-depositing into a retirement account) reinforce discipline and remove guesswork.

7. Overconfidence

It’s tempting to believe you’re that rare investor who can outsmart the market. Data suggests otherwise: studies show 97% of day traders lose money over time, and even professional fund managers often underperform indexes (Fidelity: common investing mistakes).

Common pitfalls: Overtrading, speculative bets, ignoring diversification, and failing to adapt as new information emerges. A Redditor reflected: “I thought my first few wins meant I could go all-in on options. Spoiler—it didn’t end well.”

Solution: Regularly reassess your performance with humility. Compare returns to relevant benchmarks, and be open to learning from mistakes—both yours and others’. Consider “what if I’m wrong?” for every investment decision, and size positions accordingly.

8. Neglecting to Re-evaluate Portfolio

Investing isn’t a “set it and forget it” activity. Markets, companies, and your personal goals change. Failing to review and adjust holdings can leave your portfolio misaligned. On Bogleheads, one user shared how “not rebalancing for five years meant my stocks outweighed bonds by 80/20 instead of my intended 60/40 split.”

Common pitfalls: Ignoring portfolio drift, letting winners ride without review, or failing to address changes in income, retirement plans, or market outlooks.

Solution: Schedule periodic portfolio check-ups—quarterly or annually. Adjust holdings as needed and rebalance to your target allocation. Adapt strategies if your financial situation, risk tolerance, or market conditions change.

9. Following the Crowd

Herd mentality was on full display during events like the GameStop and meme-stock craze of 2021. Social media amplifies “buy now” energy, but this crowd-following rarely ends well for latecomers. One Reddit user posted: “I YOLO’d into AMC after seeing it everywhere—now I’m down 60% and not sure what to do.”

Common pitfalls: Jumping into trends based on popularity, FOMO, or viral tips. Chasing after hot stocks or IPOs without substance or strategy. Studies of WallStreetBets discussions found increased “irrational attention [that] reduced portfolio diversification and increased correlation among speculative positions.”

Solution: Build independent convictions. Cross-check “hot” tips with personal research, and stick to your plan regardless of what’s trending.

10. Unrealistic Expectations

Many new investors mentally double their money overnight—or imagine every bet can be a lottery win. Reality is less forgiving: average market returns historically hover around 7–10% a year, and big wins are rare, as highlighted by academic studies into long-term market performance (missing the best days in the market).

Common pitfalls: Expecting 30% returns every year, betting on speculative stocks for “moonshots,” or failing to account for the risk-return tradeoff.

Solution: Educate yourself on historical averages, and set realistic benchmarks. Remember: achieving even market-like returns, over time, is an impressive and rare feat. Focus on the power of compounding, not “hitting it big.”

Table: Comparison of Costly Investor Mistakes and Solutions

| Mistake | Prevention/Remedy |

|---|---|

| Lack of Research | Deep-dive into company fundamentals before investing |

| Panic/Emotional Trades | Set investment rules and use automation to reduce emotion |

| Market Timing | Apply dollar cost averaging; stay consistently invested |

| Concentration Risk | Maintain a diversified, balanced portfolio |

| Ignoring Costs | Select low-fee funds; monitor tax impacts and account types |

| No Plan | Draft a written investment policy and stick to it |

| Overconfidence | Track performance, benchmark, seek external feedback |

| Neglecting Re-evaluation | Schedule regular portfolio reviews and adjust as needed |

| Herd Mentality | Double-check tips; trust independent research over trends |

| Unrealistic Expectations | Base returns on historical averages; avoid “get rich quick” |

Beyond-Common Sense Insights

- The cost of missing a few good days in the market is astronomical: Missing just 10 of the market’s best-performing days over 30 years can cut your total returns by more than half. Patience matters more than almost any “skill” in investing.

- Overconfidence isn’t just a beginner’s trap: Even seasoned professionals like Warren Buffett have lost billions by misjudging the risks of over-concentrating or acting too slowly (Buffett’s Letters).

- Fees on “smart” products quietly steal your compounding: Many actively managed mutual funds and variable annuities have hidden costs (e.g., 12b-1 fees, turnover) that rob investors of long-term returns, often doubling or tripling the apparent expense ratio over decades.

- Market downturns test your planning, not your IQ: Studies show the biggest differentiator for investors isn’t intelligence or analysis, but having a plan you can stick to in turbulent markets.

- Combining mistakes compounds losses exponentially: Having just two or three errors in your approach—say, overconfidence, lack of research, and poor diversification—results in underperformance far worse than any one mistake alone.

Additional Resources

- Books:

- The Little Book of Common Sense Investing by John C. Bogle

- The Intelligent Investor by Benjamin Graham

- Common Stocks and Uncommon Profits by Philip Fisher

- Online Courses:

- Morningstar Academy

- Coursera: Introduction to Finance and Accounting

- Khan Academy: Personal Finance & Investing

- Get Help:

- If you’re uncertain about crafting or refining your plan, consider consulting a reputable, fee-only financial advisor. They can help tailor strategies, avoid costly traps, and offer behavioral coaching when nerves get tested.

Conclusion

Looking back, I realize how many of my own market mistakes were completely avoidable—if only I had paid more attention to these principles. The common theme across everyone’s stories, including mine, is that no one is immune to the psychological traps, hasty decisions, or overlooked fees that quietly hurt investment returns. But with patience, an honest review of your habits, and a plan based on fundamentals—not just hope or hype—you can steadily avoid the errors that cost investors so much money.

Let’s recap the step-by-step process I outlined above:

- Start with thorough research and only invest in businesses you genuinely understand.

- Set written, long-term goals—and stick to them, even when emotions run high.

- Total market timing is a mirage; consistent, patient investing nearly always wins.

- Keep your portfolio diversified and your costs low—these two habits alone put you ahead of most participants.

- Revisit your plan and allocations regularly, benchmarking and adjusting as life changes.

- Do not be swayed by noise or the latest trend, and always ground your expectations in reality.

Remember, you don’t have to be perfect—just avoiding the biggest pitfalls makes a world of difference over time. I invite you to share your own experiences or questions in the comments: what’s the most expensive mistake you’ve made (or avoided)? Let’s help each other build stronger, smarter investment habits and keep more of the wealth we work so hard to earn.