I’ve spent years experimenting with different ways of generating income from investments, but again and again, dividend investing proves itself uniquely powerful for building steady passive income. Dividend investment generates passive income by letting you share in company profits, turning your portfolio into a reliable cash machine—one that requires patience, planning, and a clear strategy. In this article, I’ll break down how dividend investing works, why it can be such a game-changer, and, most importantly, my complete, step-by-step strategy for achieving regular returns in any market—for retirees and young accumulators alike.

Quick Summary

- Dividend investments provide regular passive income by sharing profits from stable companies.

- Yields, payout ratios, and dividend growth are central to selecting quality stocks.

- Reinvesting dividends enables compounding, transforming small sums into substantial income over decades.

- Portfolio diversification—across sectors, yields, and “Dividend Aristocrat” stocks—mitigates risks.

- Tax efficiency and choosing the right investment accounts maximize after-tax returns.

- Adjusting your dividend strategy as markets or your life changes ensures consistent, sustainable income.

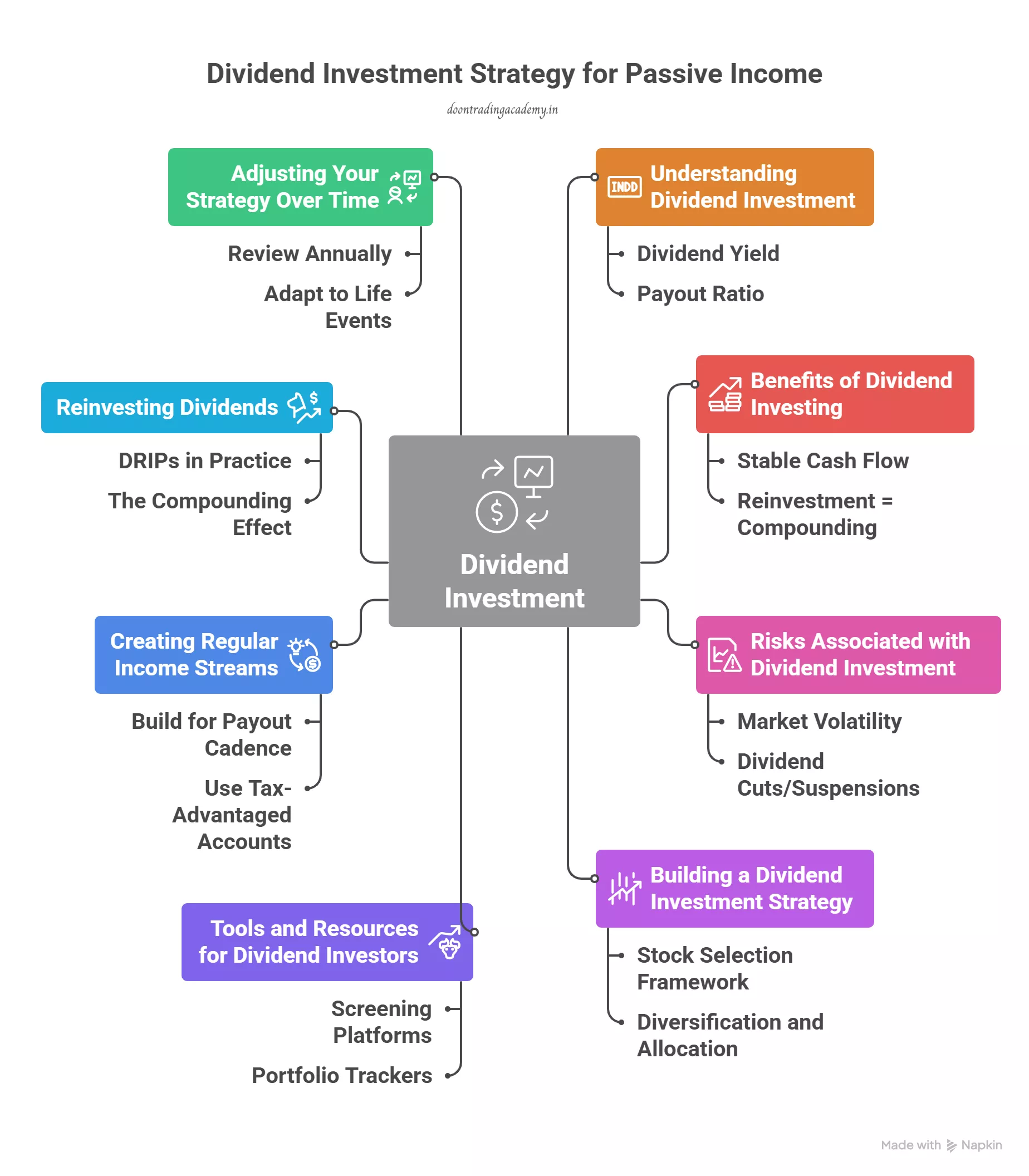

1. Understanding Dividend Investment

Dividend investing is about collecting regular payouts—called dividends—that companies share from their profits. Instead of banking solely on stock price growth, you aim to build an income stream that grows with time. Dividends most often come as cash, but can also be extra shares (stock dividends). As an investor, you monitor a company’s dividend yield—the ratio of annual dividends to the stock price—to compare income potential across stocks or funds.

For example, a $100 stock that pays $3 a year in dividends has a 3% yield. But yield isn’t the only factor; you need to assess the company’s payout ratio (what percent of profits they pay out), balance sheet health, and history of maintaining or growing the dividend. Safety is crucial: “A dividend is only good if it’s sustainable,” as the Reddit user DividendGuy92 wisely noted. I always look for payout ratios below 60% and prioritize companies that have raised payouts over multiple business cycles.

Types of Dividends

- Cash dividends: Regular payments (most common—quarterly or monthly).

- Stock dividends: Additional shares instead of cash.

- Special or one-time dividends: Unscheduled, from excess profits or asset sales.

The Role of Yield

Dividend yields vary by sector and market conditions. Between 2–5% is typical for established “safe” stocks. Yields over 6% may signal risk—sometimes a “yield trap” where the price falls due to looming trouble, as experienced by many holders of high-yield REITs in 2023.

| Term | Definition |

|---|---|

| Dividend Yield | Annual dividends per share ÷ current stock price |

| Payout Ratio | Percent of earnings paid as dividends |

2. Benefits of Dividend Investing

Dividend investing’s main appeal is dependable passive income—even in flat or down markets. Here’s why seasoned investors (and, admittedly, myself) love this approach:

- Stable cash flow: Quality companies like Realty Income and Procter & Gamble have raised dividends through recessions, market shocks, and inflation spikes.

- Reinvestment = compounding: Automatically reinvested dividends buy more shares, creating a “dividend snowball.” I’ve witnessed firsthand how even $100/month quickly becomes $1,000/year if you stick to a DRIP plan.

- Tax benefits: Qualified dividends are taxed at lower capital gains rates (0%, 15%, or 20%), not ordinary income rates[23]. This can mean thousands saved versus interest income or non-qualified dividends (like those from REITs, certain preferred stocks, and MLPs).

- Inflation-beating income: S&P 500 dividends have historically grown faster than inflation—5.77% annual dividend growth vs. 3.13% average inflation since 1979[24]. Your payout power increases over time, protecting your spending ability.

- Total return advantage: Academic studies and real-world examples show that about 40% of long-term stock market gains come from reinvested dividends.

3. Risks Associated with Dividend Investment

It’s tempting to chase fat yields, but dividend investing has real pitfalls:

- Market volatility: Share prices can fall—even the best dividend stocks aren’t immune to bear markets. While your income may hold steady, your portfolio value can swing dramatically.

- Dividend cuts/suspensions: Companies in trouble may slash payouts overnight (think GE, or many REITs in 2020), turning reliable income into disappointment. Redditor IncomeHunter put it best: “A cut hurts twice—your income drops, AND the share price tanks.”

- Yield traps: A too-good-to-be-true yield is usually a warning. As Morningstar research indicates, yields over 7% are often unsustainable, especially if the payout ratio approaches or exceeds 100%[19].

- Sector concentration: Banks and energy stocks, for example, may have tempting dividends but are highly cyclical—2020 was a reminder how quickly dividends can disappear in tough sectors.

- Tax mismatches: If you hold non-qualified dividend stocks in taxable accounts, you could see your after-tax income slashed—always consider “asset location” when building your portfolio.

4. Building a Dividend Investment Strategy

This section lays out the process I use and recommend for constructing a resilient dividend portfolio, regardless of your starting point:

Stock Selection Framework

- Analyze dividend yield: Target reliable companies in the 2–5% range, or above average for sector.

- Examine payout ratios: Avoid stocks routinely paying out more than 70% of earnings—these are prone to cuts when profits dip.

- Check the dividend history: Seek businesses with a long, unbroken record of maintaining (and preferably increasing) dividends through various cycles. The Dividend Aristocrats (25+ years of dividend growth) are an ideal pool. Kings (50+ years) are the ultimate.

- Study company financials: Look at debt load, cash flows, and profitability trends.

Diversification and Allocation

A robust portfolio isn’t built on one or two stocks. Allocate across sectors—consumer staples, healthcare, utilities, industrials, and a handful of REITs or high-yielders. For example, I aim for 15–30 stocks, with no more than 10% in a single holding. ETFs like SCHD or VYM can be core components for instant diversification.

| Strategy | Best For |

|---|---|

| Dividend Growth | Building wealth, beating inflation, long-term income increase |

| High Yield | Immediate larger income, but usually slower growth, higher risk |

“Don’t put all your eggs in one basket—even in dividend investing” is advice echoed often on subreddit r/dividends and in forums like Bogleheads, and I’ve learned this truth the hard way. Smart diversification keeps your income flow steady even if one stock falters.

5. Tools and Resources for Dividend Investors

- Screening platforms: Tools like Dividend.com, Simply Safe Dividends, and stock screeners at major brokerages let you filter stocks by yield, payout ratios, growth history, and sector.

- Portfolio trackers: Services like TrackYourDividends.com and built-in brokerage tools help monitor dividend schedules, cash flow, and reinvestments.

- Online communities: The Reddit r/dividends community is a gold mine of real-world experiences, portfolio critiques, and troubleshooting help—“Posting my $10K dividend portfolio for feedback was the single most helpful thing I did,” writes user DivLad23.

- Financial news and research: Websites like The Motley Fool and Morningstar provide deep analysis and risk reviews of dividend stocks and funds.

Five Beyond-Common-Sense Dividend Investing Facts

- Yields above 8% are almost always a red flag, not “found money”—often a sign of looming trouble, not opportunity.

- Dividend “quality” matters more than yield; many Aristocrats and Kings offer lower yields but far stronger long-term results thanks to years of consistent growth.

- Realty Income (O) is one of the few stocks paying monthly dividends and has increased its payout for over 56 years, making it a favorite among those seeking monthly income.

- Reinvesting even small dividends over decades can turn an initial $5,000 into $170K+, illustrating compounding’s real-life power.

- Tax location (where assets are held) can impact your income by 1–2% per year—holding REITs inside IRAs and qualified dividend stocks in taxable accounts is a savvy tactic that significantly boosts after-tax returns.

6. Creating Regular Income Streams

To produce steady, predictable dividend income, it’s not enough to simply “buy dividend stocks.” Here’s what I recommend:

- Build for payout cadence: Select a mix of quarterly, monthly, and (less common) semiannual payers. Funds like SCHD pay quarterly, whereas Realty Income and STAG Industrial pay monthly.

- Spreading payments: Map ex-dividend and pay dates so income arrives throughout the month—not all in one quarter. Some investors use a “Dividend Calendar” to pace expenses.

- Use tax-advantaged accounts: When possible, stash your highest-yield or non-qualified dividend holdings (like REITs) in IRAs or Roth IRAs. This keeps more of your income away from the IRS.

- Balance yield vs. growth: Don’t overweight on high-yielders that risk future cuts. Blend in steady growers (“dividend growth investing”) to future-proof income.

7. Reinvesting Dividends

I can’t overstate this: consistently reinvesting dividends (using DRIPs—Dividend Reinvestment Plans) is the ultimate “secret sauce” of growing regular income:

- DRIPs in practice: Nearly all brokers now offer automatic, fee-free reinvestment. You don’t have to lift a finger—your dividends buy more shares, which then earn more dividends.

- The compounding effect: Let’s say you invest $5,000 in a mix of 3% yielders. By reinvesting, you might grow that to $24,000 in 10 years, and over $170,000 in 30 years, generating over $2,000/month in income[2][54]. The “dividend snowball” turns your portfolio into an income engine.

- Automatic vs. manual reinvestment: Some investors prefer to collect dividends and buy new opportunities (“strategic reinvestment”). For most, automating the process removes emotion and inconsistency.

In my own experience, the psychological boost of seeing rising dividend income—even in rough markets—makes it easier to stick with the plan. It’s a proven behavioral “glue” for long-term investing discipline.

8. Adjusting Your Strategy Over Time

Successful dividend investing is not a “set-it-and-forget-it” game. Here’s how I—along with many in the r/dividends community—keep my returns regular as life changes:

- Review annually: Examine portfolio yield, payout ratios, sector weights, and growth rates at least once a year. Make changes if a company’s fundamentals crack or if it signals a dividend cut.

- Monitor company news: Sometimes a dividend is “safe” one year and on the ropes the next. Stay informed via news feeds and earnings calls, not just static numbers.

- Adapt to life events: As you near retirement or require higher income, consider shifting toward higher-yield stocks or funds—gradually. Young investors should prioritize growth; retirees might want more cash flow.

- Plan for withdrawals: Decide when to stop reinvesting and start “spending” dividends—ideally after your snowball has grown large enough to fund your needs.

- Stay diversified and tax-aware: As your holdings grow, rebalance to avoid portfolio drift, and check that new investments are in the optimal account type for taxes.

Remember, regular monitoring is about opportunities and risk control—not obsessive trading. As Redditor DividendDynamo notes, “The biggest mistake is falling asleep at the wheel—companies, and life, change.”

Conclusion

In my experience, dividend investment genuinely generates passive income—enabling freedom and flexibility I haven’t found elsewhere in the market. Building a dividend portfolio isn’t about chasing the highest yields or making big, fast moves. Instead, it’s a process: start with quality stocks or ETFs, focus on consistent (not spectacular) yields, reinvest dividends for years, and keep monitoring your mix as your goals and the market evolves.

To recap, the actionable step-by-step strategy looks like this:

- Set your income goals and time horizon.

- Research and select a mix of dividend stocks and/or funds, prioritizing safety, growth, and diversification.

- Use tools and community resources to track yield, payout ratio, and dividend safety.

- Reinvest all dividends, letting the snowball grow.

- Regularly review and rebalance your portfolio as companies or your needs change.

- Optimize your account types for taxes and payout scheduling for smooth income.

Dividend investing is a marathon, not a sprint. The discipline of reinvesting—combined with patience and strategic adjustments—can turn modest beginnings into life-changing income down the road. I’d love to hear your experience, questions, or favorite dividend strategies—drop a comment or share your own story below so we can learn together. Your journey to regular passive income can start today!