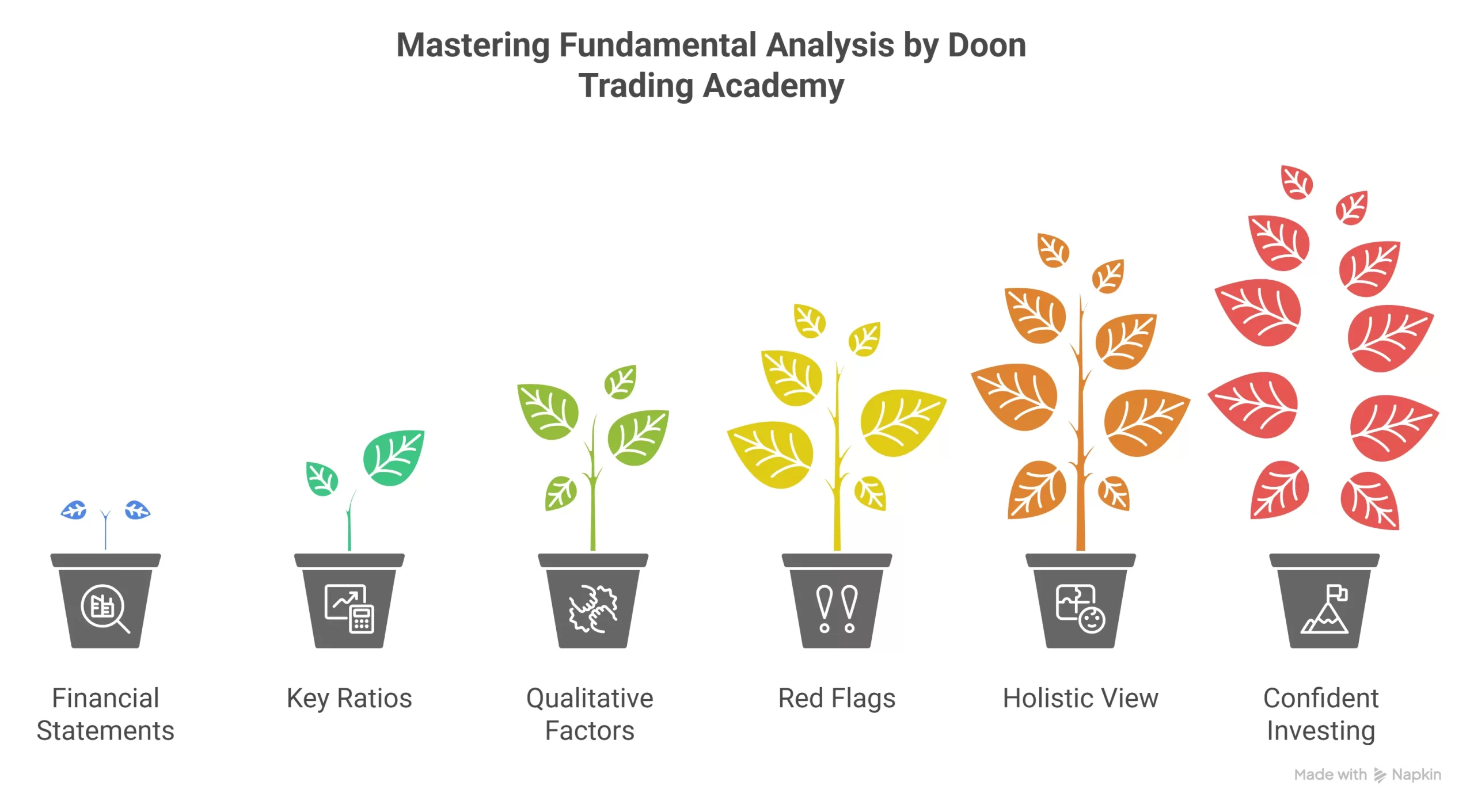

As someone who has navigated the complexities of investing, I know firsthand how overwhelming it can be when you’re trying to figure out if a company’s stock is truly worth your hard-earned money. Fundamental analysis is the tool that helped me cut through the noise and assess real-world company value, beyond hype and short-term trends. It involves studying the actual business, its numbers, and the people behind it, so you can make smarter, long-term investment choices.

In this article, I’ll walk you through beginner-friendly methods that form the backbone of fundamental analysis. You’ll learn how to read financial statements, interpret the most common valuation ratios, and apply practical, proven techniques—so you can approach investment decisions with confidence, not guesswork.

Quick summary

- Fundamental analysis focuses on a company’s real value, not just its share price movements.

- It uses financial statements and ratios like P/E, EPS, ROE, Debt-to-Equity, and the Current Ratio to judge health and worth.

- Unlike technical analysis, it is based on business fundamentals for long-term strategy.

- Practical methods include deep-diving into numbers, comparing with peers, and assessing management quality.

- Learning these tools sets a solid foundation for successful investing and helps avoid common beginner mistakes.

Understanding Fundamental Analysis

Fundamental analysis is a method investors use to evaluate a company’s true worth based on its underlying business performance rather than just share price movements. The main goal is to determine whether a stock is undervalued or overvalued by the market, so you can make smart investment decisions.

This approach contrasts with technical analysis, which is more concerned with charts and trends driven by market psychology. Fundamental analysis digs deeper, examining real business data and long-term prospects. According to Charles Schwab, it helps answer a simple question: “Is the company healthy?” This method is a core component for long-term investors, as it clarifies whether a business can withstand downturns and continue to de.r value to shareholders.

Analyzing Financial Statements

Financial statements are the building blocks of fundamental analysis. By learning to read them, you get a window into how a company actually operates and makes money. The three key statements are:

- Balance Sheet: Shows what the company owns (assets) and owes (liabilities) at a given point, revealing its financial stability and liquidity. As many investors say, “Cash is king” because strong cash reserves mean the business can survive tough times.

- Income Statement: Details the company’s revenues, expenses, and profits over a period. You can spot growing revenues, profit margin trends, and unusual expenses that require deeper investigation.

- Cash Flow Statement: Tracks the actual cash moving in and out. Unlike profits, cash can’t be faked—this shows what’s really happening behind the scenes.

My early investing years taught me that numbers can lie if you only skim the surface. For instance, a company might post big profits, but digging into its cash flows could reveal it’s actually burning through cash just to keep going. Always analyze these statements together for a full picture.

| Statement | Key Insights |

|---|---|

| Balance Sheet | Financial health, solvency, asset base |

| Income Statement | Profitability, growth trends, cost control |

| Cash Flow Statement | Liquidity, sustainability, real earnings |

Price-to-Earnings (P/E) Ratio

The P/E ratio is one of the most quoted numbers in investing—and for good reason. It tells you how much the market is willing to pay for $1 of a company’s earnings. The formula is simple:

- P/E Ratio = Current Share Price ÷ Earnings Per Share (EPS)

A high P/E might suggest investors expect strong growth; a low P/E could signal that a stock is undervalued or there are concerns about its future. For instance, as u/stoicanalyst from Reddit put it: “Apple’s low P/E in 2016 scared some people off, but those who understood the fundamentals doubled their investment.”

It’s crucial to compare P/E ratios with similar companies in the same sector and with the company’s own history—what’s ‘high’ for a utility may be ‘normal’ for a tech giant.

| P/E Range | Common Interpretation |

|---|---|

| High (25+) | Growth expected, or possibly overvalued |

| Low (<15) | Potential value or underlying problems |

Pro tip: Use the forward P/E (based on future earnings) for a more up-to-date outlook, but remember these are based on analyst forecasts, which aren’t always reliable.

Earnings Per Share (EPS)

EPS breaks down profits for each share, letting you see how profitable a company really is per stock you own:

- EPS = Net Earnings ÷ Number of Outstanding Shares

A rising EPS over time signals the company is growing profits—a healthy sign. By tracking EPS trends over several years, you can spot consistent growth or worrying declines. In my experience, a company with stagnating or falling EPS is a red flag that warrants further digging.

Investors on Stocktwits often share this sentiment. As @growthhunter2020 wrote, “Watching EPS growth quarter by quarter has kept me from holding on to zombie stocks.”

Return on Equity (ROE)

ROE measures how efficiently a company uses shareholders’ money to produce profit. The formula:

- ROE = Net Income ÷ Shareholder’s Equity

A higher ROE means better management performance and often signals a competitive edge. Generally, an ROE between 15% and 20% is considered strong, but it’s important to compare with industry averages since capital requirements vary.

User InvestorNewbie99 shared on Bogleheads: “I learned the hard way—very high ROE isn’t always good. Sometimes it’s artificially boosted by lots of debt.”

This highlights the importance of cross-checking ROE with debt levels; if a company uses heavy borrowing, its ROE can look artificially impressive while risk shoots up.

Debt-to-Equity Ratio

This ratio reveals how much of the company’s financing comes from debt versus shareholders’ equity:

- Debt-to-Equity = Total Debt ÷ Total Equity

A low ratio (typically under 1) means the company isn’t overly reliant on borrowing, which is safer in downturns. However, some industries (like utilities or telecoms) operate with higher ratios due to capital needs.

As I discovered in my own practice, too much debt can turn small setbacks into crises. That’s why investors on Wall Street Oasis often suggest, “Don’t just look at growth—check the D/E ratio so you don’t get blindsided if financing dries up.”

| Debt-to-Equity Ratio | Interpretation |

|---|---|

| < 1 | Conservative, safer, less financial risk |

| 1 – 2 | Moderate, typical for some industries |

| > 2 | High leverage, elevated risk |

Current Ratio

The current ratio evaluates a company’s liquidity—its ability to pay short-term bills:

- Current Ratio = Current Assets ÷ Current Liabilities

A value above 1 signals there’s enough current assets to cover obligations. A number below 1 could mean the company faces cash flow problems soon. But an extremely high current ratio may indicate excess, underutilized assets.

In my experience, the current ratio serves as an early warning system. As user ValueVeteran commented on a popular forum: “I skip any stock with a current ratio under 1—too risky during a downturn.”

Beyond the Basics: Advanced Insights and Real-World Application

- Discounted Cash Flow (DCF) Analysis gives a direct estimate of intrinsic value. As experts highlight, “It’s not a point estimate—think in value ranges” (QuintEdge).

- The P/E ratio and other multiples can look misleading alone—always benchmark against industry peers and historical averages to find true context.

- Analyzing qualitative factors (like management quality and competitive moats) is crucial. As pointed out in the Financial Modeling Prep API, “Management and corporate governance can make or break company fortunes.”

- Financial statement analysis involves more than ratios—look for quality of earnings by checking if net income matches cash flow from operations, exposing any accounting trickery.

- Combining fundamental with industry and macroeconomic trends (e.g., regulation or innovation impacts) provides a holistic perspective.

Many investors initially struggle, but as statistics from investment communities show, mastering these five methods leads to far better long-term results—the difference between guessing and investing with conviction.

Common Pitfalls and Troubleshooting (From My Experience)

- Avoid relying on a single ratio or number. I used to focus on just EPS or P/E, missing the big picture. Context is always key.

- Don’t neglect industry specifics. A “normal” debt ratio for a tech firm could be disastrous for a retailer, and vice-versa.

- Beware of accounting tricks. Net profit can be manipulated; cash flow is much harder to fake. Always cross-check earnings with cash flows.

- Stay objective and patient. It’s easy to get caught up in hype or panic. Fundamental analysis is about the long game, not quick wins.

- Step back when confused. I’ve learned that if the numbers are too good to be true or too complex to understand, I’ll walk away—there are always simpler, safer opportunities out there.

As u/stocksage posted on Reddit, “My best decisions came from sticking to these basics and ignoring the crowd noise.

Additional Resources

- The Intelligent Investor by Benjamin Graham

- Charles Schwab’s guide to Fundamental Analysis

- Coursera Fundamentals of Finance course

- ValuePickr Forums and Bogleheads – Learn from experienced investors

- Check out free tools such as Yahoo Finance, Morningstar, and Thinkorswim for hands-on analysis.

Conclusion

In my experience, getting started with fundamental analysis completely changed the way I invest. By focusing on the real numbers, understanding where a company’s profits come from, and steadily learning to interpret key ratios, I moved from guessing to making confident, long-term decisions.

Recap of the step-by-step process:

- Start by digging into company financial statements—learn their language and look for trends across years.

- Apply key ratios like P/E, EPS, ROE, Debt-to-Equity, and Current Ratio to compare companies and peer groups.

- Analyze both the numbers and qualitative factors—management, industry strength, and business model fit.

- Check for any red flags or discrepancies, and always use more than one metric for a balanced view.

- Keep learning and adjust your approach as you gain experience, using community resources for support and continuing education.

If you’re a beginner, invest the time to master these methods—they form the foundation for smart investing, whether you manage your own portfolio or simply want to make sense of stock recommendations. Do you have questions, tips, or personal experiences with fundamental analysis? Leave a comment below—I’d love to hear your perspective and help you along the way.