Understanding how to invest is one of the most important financial skills you can develop. Whether you’re looking to build long-term wealth or simply want a smarter way to grow your savings, choosing the right investment vehicle is crucial. Mutual funds and stocks are two of the most popular options for individual investors, yet they operate quite differently. In my experience, successfully navigating the choice between mutual funds and stocks calls for a clear grasp of their core distinctions—not just surface-level advice.

This article will walk you through eight key differences every investor must understand in the mutual funds vs stocks debate. I’ll share both research-backed insights and real-life experiences (including some confessions from seasoned investors) so you’ll have the context and confidence to decide which approach fits your goals, time, and temperament.

Quick Summary

- Stocks offer direct company ownership and voting rights, while mutual funds pool money to buy a basket of securities.

- Mutual funds de.r instant diversification with a single purchase; stocks require manual selection and portfolio building for similar risk reduction.

- Fees for mutual funds (especially actively managed) can erode returns over time; stock investors face market commissions but less recurring expense.

- Mutual fund trading executes once daily at NAV; stocks trade instantly during market hours, allowing rapid buy or sell decisions.

- Mutual fund investors encounter capital gains distributions regardless of selling; stock investors can precisely control when they realize gains.

- Professional managers run mutual funds, making them lower-maintenance; stocks demand ongoing research and monitoring.

- Stocks may offer higher upside or volatility, while mutual funds smooth out results via diversification.

- The optimal strategy for most is a mix—using low-cost index funds as a core and stocks for specialized bets if you have time and expertise.

1. Definition and Structure: Direct Ownership or Pooled Investment?

Let’s start with the basics. Buying an individual stock means you’re purchasing a fractional share of a real company—imagine holding a small slice of Apple or Ford. This ownership entitles you to a portion of its profits and (sometimes) voting rights on company matters. As Investopedia succinctly puts it: you’re betting directly on a company’s prospects and can buy or sell at your discretion during market hours.

Mutual funds, on the other hand, are “baskets” of investments managed by professionals. When you invest in a mutual fund, you aren’t buying pieces of each company directly. Instead, you own a share of the fund, which in turn owns shares (or bonds, or combinations) of different underlying assets. This structure means your “ownership” is one step removed from the actual companies—your returns are tied to the fund’s overall performance, not just a single stock. Control is delegated to a fund manager or an automated tracker in the case of index funds.

| Stocks | Mutual Funds |

|---|---|

| Direct ownership in one company; voting rights for some stocks. | Pooled ownership in a portfolio; no voting rights on companies. |

On Reddit’s r/personalfinance, user toofiftyeight summarized: “With stocks, you’re captain of your ship. With mutual funds, you’re a passenger—someone else is charting the course.”

2. Ownership and Control: How Much Say Do You Get?

Owning stocks puts you in control—you can decide what to buy and when to sell, set stop losses, participate in shareholder meetings (if you hold enough), and customize your individual portfolio. This hands-on approach appeals to investors who want a seat at the table or feel confident in their company analysis skills.

Mutual funds flip that dynamic. You have no control over day-to-day trades within the fund, which can be both a blessing (professional risk management) and a frustration (lack of influence on holdings). Fund managers make active decisions about which stocks to buy, hold, or sell, following their stated strategy. Some index funds are even managed algorithmically with zero human intervention. As Bogleheads investors often discuss, for those preferring to “set it and forget it,” this delegation can be a huge advantage.

3. Diversification: Single Company Bets or Broad Exposure?

If you invest in a single stock, your outcome depends almost entirely on just that company. Hit the jackpot with the next Apple or Tesla, and you’ll see outsized gains—but the risks are equally large. To offset this, experienced investors build “baskets” of stocks spanning industries, sizes, and geographies. But assembling a diversified portfolio from scratch takes research, time, and sometimes a hefty bankroll.

Buying a mutual fund achieves instant diversification in one step. For example, a basic S&P 500 index fund gives exposure to 500 leading U.S. companies across all sectors. As research published by the FINRA Foundation shows, that diversification reduces the volatility (sudden ups and downs) you’d experience compared to holding just a single stock or a small group of stocks. It’s the reason why Warren Buffett famously recommended most investors stick with low-cost index funds.

| Stocks | Mutual Funds |

|---|---|

| Potential to diversify, but requires picking and managing multiple stocks. | Instant diversification across dozens or hundreds of assets in one fund. |

A forum user lazard98 wrote, “It only took one earnings miss to realize I shouldn’t be betting my future on a single company. Switched to index funds and sleep a lot better.”

4. Risk and Return: What’s the Volatility Trade-Off?

With stocks, there’s no ceiling—and no floor. Pick the right company at the right time and your returns could far outpace any diversified fund. But as shown in research by Arizona State Professor Henrik Bessenbinder, a tiny s.r of stocks drives most market gains; the majority underperform Treasury bills over time. For many, that means the odds are stacked against consistent outperformance via individual stock picking.

Mutual funds, thanks to their diversified structures, spread risk across many holdings. While that limits the explosive upside you could see with a single winning stock, it also protects you from catastrophic losses if one company implodes. According to a recent S&P Global report, only 22% of active U.S. mutual fund managers beat their benchmark over ten years, emphasizing the difficulty of “beating the market” even for pros.

If you’re comfortable with higher volatility and are disciplined enough to hold through major swings, stocks could de.r bigger results. If you prefer steadier growth and lower swings, mutual funds—especially broad-market index funds—are designed for you.

5. Fees and Costs: The Hidden Wealth Erosion

One of the most disruptive differences between mutual funds and stocks is the way fees are charged—and how those costs compound. Stocks themselves don’t have ongoing fees; you only pay your broker when you buy or sell (and today, many major online brokers have slashed commissions to zero for U.S. stocks).

Mutual funds, by contrast, come with “expense ratios”—annual fees paid to cover management, administration, and sometimes marketing. While index funds often keep these below 0.10%, actively managed mutual funds may take 0.5% to over 1% per year. Across decades, even a 1% fee can substantially reduce your wealth: according to Vanguard, a 1% annual fee could eat up tens of thousands of dollars in retirement savings for an average investor.

| Stocks | Mutual Funds |

|---|---|

| Pay commissions when buying/selling (often $0 with modern brokers). No annual fee. | Annual expense ratios deducted from returns; may include sales loads or redemption fees. |

A Redditor, IgnatiusFinance, commented: “I switched from managed funds to ETFs and literally saw my fees drop 80% overnight.”

6. Management and Expertise: Professional Oversight or DIY?

Owning stocks means you’re in the driver’s seat—you perform the research, identify opportunities, and make every buy/sell decision. For many, this is the appeal: the chance to use your judgment and (hopefully) outperform the market.

Mutual funds assign these tasks to a professional manager (active funds) or an algorithm (passive/index funds). This can be a double-edged sword: you benefit from someone else’s expertise and full-time focus, but you’re also trusting they can de.r results worth the fees.

Numerous studies, including S&P’s annual SPIVA report, reveal that most professional managers fail to consistently outperform simply “owning the market” through low-cost index funds. That’s why many seasoned investors—like CFA Elizabeth Holmenlund—choose market-tracking ETFs for their personal portfolios, citing the near impossibility of beating the system after costs.

7. Liquidity and Accessibility: When Can You Trade?

Stocks offer premier liquidity—trades can be executed virtually instantly during market hours at market prices. This makes stocks suitable for investors who want to actively manage positions or need immediate access to cash.

Most mutual funds, by contrast, only process trades once per day after the market closes. Your purchase or sale price is the fund’s net asset value (NAV) calculated at that day’s end. If sudden news breaks at 2 p.m., you’ll have to wait until the daily close for your trade to go through.

| Stocks | Mutual Funds |

|---|---|

| Trades executed instantly during market hours. | Trades processed after market close at daily NAV; no intraday trading. |

ETFs (exchange-traded funds), which are a subcategory of funds, trade like stocks—so if you want the best of both worlds (diversification and intraday liquidity), ETFs might be a good fit.

8. Tax Implications: Capital Gains Complexity

Taxes can get surprisingly tricky with mutual funds. When a mutual fund manager sells a security at a profit, the IRS requires the fund to distribute realized gains to all shareholders—even those who only recently purchased shares. This can trigger “phantom” tax bills regardless of whether you personally sold any of your investment. New investors may even owe tax on gains from before they bought in, a scenario tax experts call “inherited gains.”

Owning stocks directly lets you control exactly when you realize gains or losses, making it easier to implement tax-saving strategies like tax-loss harvesting or charitable donations of appreciated shares. ETFs offer more favorable tax treatment compared to mutual funds due to their unique structure, often avoiding capital gains distributions entirely.

If you’re investing via a tax-advantaged account like an IRA or 401(k), these issues are less relevant since all gains grow tax-deferred.

| Stocks | Mutual Funds |

|---|---|

| You control when to realize capital gains. | Fund may distribute capital gains, triggering taxes even if you didn’t sell. |

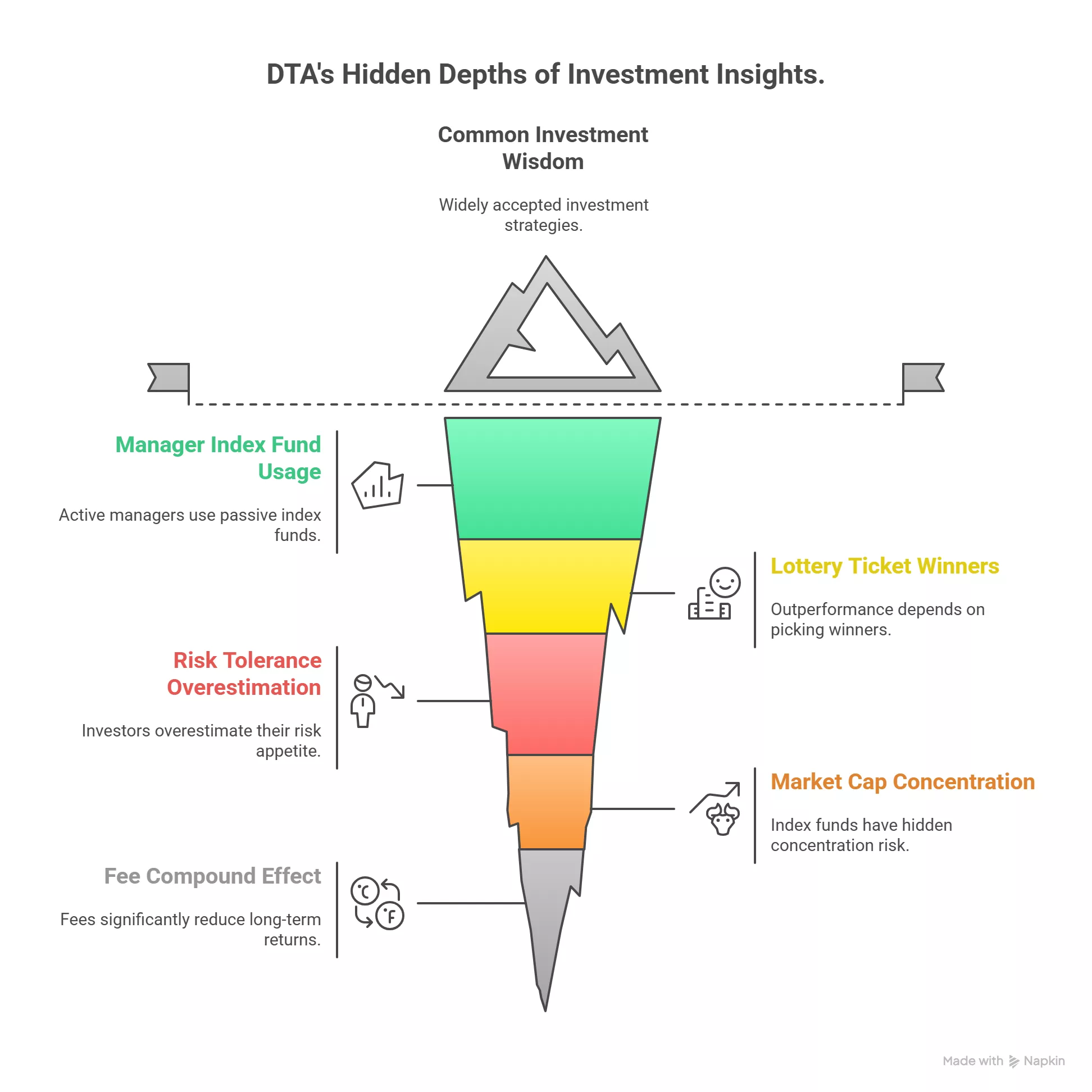

5 Advanced & Beyond-Common-Sense Insights

- The most successful active managers still use index funds in their personal portfolios. Even top-rated fund managers (like those tracked by Morningstar) admit the “set it and forget it” approach with low-cost index funds often beats trying to outsmart the market.

- Long-term outperformance in stocks depends on catching “lottery ticket” winners. Research from Professor Bessenbinder shows that a tiny number of companies have contributed the majority of market returns—meaning picking even one wrong company can devastate your strategy.

- Stock investors regularly overestimate their risk tolerance. “You only know your true risk tolerance when the market tanks,” as one forum user pointed out. During downturns, panic selling is far more common among unprepared stock investors than those in diversified funds.

- Index funds and ETFs aren’t entirely passive—market cap weighting can lead to hidden concentration risk. In 2023–2025, the “Magnificent Seven” stocks (like Nvidia and Apple) made up over 30% of the S&P 500 index, increasing single-stock exposure within an apparently diversified fund.

- Fees compound over time more than you expect. According to Vanguard, every additional 1% annual fee can cut your retirement nest egg by over 20% across 30 years. What seems small now balloons in the long run.

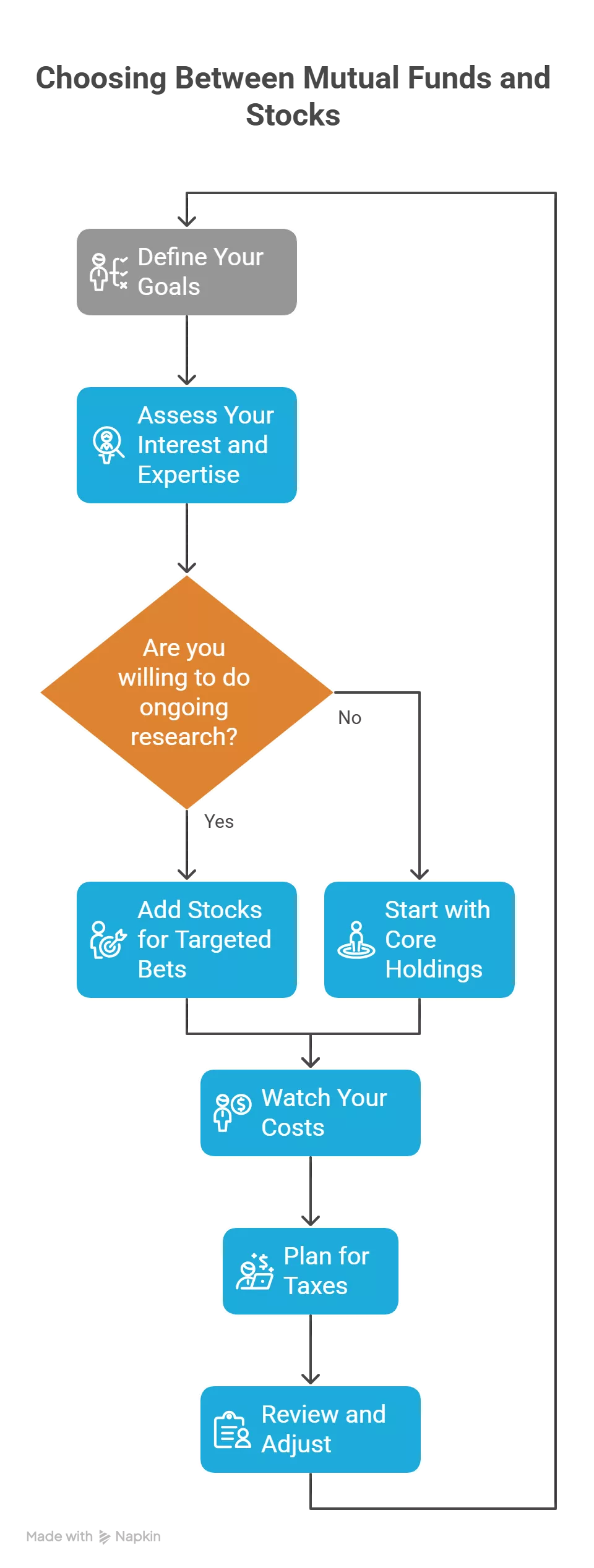

Conclusion: What This Means For Your Investing (Step-by-Step Recap)

After years of investing in both mutual funds and individual stocks, I’ve realized no one-size-fits-all answer exists. The choice comes down to balancing control, effort, risk, and cost with your personal goals and temperament. Here’s how I recommend approaching this—step by step:

- Define your goals: Is rapid growth, steady income, or capital preservation more important?

- Assess your interest and expertise: Are you willing and able to do ongoing research and handle emotional swings?

- Start with core holdings: For most people, build the foundation with broad, low-cost mutual funds or ETFs.

- Add stocks for targeted bets: If you want more upside and are willing to dig deep, set aside a limited portion for individual stocks.

- Watch your costs: Use the lowest-fee options available; high expenses quietly eat away at gains.

- Plan for taxes: Be aware of potential surprises from fund distributions or realized stock gains.

- Review and adjust: Check your portfolio’s balance and performance yearly, always keeping your original strategy in mind.

In the end, mutual funds vs stocks isn’t a battle—it’s about creating the right blend for you. Personally, I find peace of mind in combining the “set it and forget it” safety of index funds with a handful of individual stocks for excitement and higher reward potential. What matters is that you use the strengths of each tool to serve your long-term financial future.

What do you think—are you more comfortable with mutual funds, taking your chances with stocks, or mixing both? Share your own experiences or questions in the comments below; I’d love to hear your perspective!