When I started exploring ways to build wealth in India, the buzz around SIPs (Systematic Investment Plans) kept surfacing—especially when coupled with the concept of Rupee Cost Averaging. At first, these financial terms sounded intimidating, but the more I learned (and experienced), the clearer it became: Discipline and method always outpace lucky guesses or market timing. In this complete setup guide, I’ll walk you through why SIP investments are trusted by millions, how rupee cost averaging silently works for you, and most importantly—how you can set up your own step-by-step plan for long-term wealth creation.

Quick summary

- SIP stands for Systematic Investment Plan—regularly investing a fixed amount in mutual funds.

- Rupee cost averaging helps counter market volatility by spreading investments across price highs and lows.

- Historical cases prove disciplined SIPs can turn modest monthly amounts into multi-crore portfolios.

- Long-term wealth grows exponentially due to compounding and consistent contributions.

- A successful SIP setup needs clear goals, proper fund selection, and emotional discipline.

Introduction to SIPs and Rupee Cost Averaging

To put it simply, a SIP allows investors to channel funds into chosen mutual funds at fixed intervals (usually monthly). Rather than trying to “time” the market—something even professionals rarely get right—SIPs help you ride through both market peaks and troughs. Fundamentally, what makes SIPs powerful is Rupee Cost Averaging (RCA): this approach buys you more units when markets are low and fewer when prices are high, effectively lowering your average acquisition cost over time.

1. Understanding SIP Investment

A SIP isn’t a product—it’s an investment strategy tailored for those who want to build wealth, minimize risk, and maintain discipline without watching the market every day.

- Definition: SIP is an approach where you invest a fixed sum at pre-decided intervals (mostly monthly or quarterly), buying units of your selected mutual fund.

- Key Features: Automates investment, lowers entry barriers (many start at ₹500/month), and simplifies the process.

- Benefits: Instills habit, leverages compounding, and avoids lumpsum market timing.

| SIP Investment | Lumpsum Investment |

|---|---|

| Fixed, regular contributionsReduced risk from market ups/downsDisciplined approach | One-time, large outlayHigh risk if mistimedRequires timing skill |

Reddit user u/serendipitypie shared: “Started a ₹3k/month SIP back in 2014—watched it fall, rise, fall again. 8 years later, it’s worth ₹8.9 lakhs on ₹2.8 lakhs invested. Never thought slow and steady would win.”

2. The Concept of Rupee Cost Averaging

Rupee Cost Averaging is elegantly simple—by investing at fixed intervals, you buy more mutual fund units when prices are low and fewer when prices are high. Over the years, this smooths out the average cost per unit and helps avoid the stress of catching market highs or lows.

- How it works in SIPs: Each investment buys units at prevailing prices. Over time, market fluctuations result in different units purchased for the same amount.

- Primary benefit: Naturally reduces purchase price risk, especially in volatile markets.

- Smart during corrections: Frequent market dips actually favor SIP investors.

As noted by u/arun_invests on a Reddit thread: “I kept my SIP going through both 2008 and 2020 crashes—watching the NAV tumble was terrifying, but compounding and RCA made me grateful for not pausing.”

3. Wealth Creation through SIP and Rupee Cost Averaging

There’s a reason so many financial planners and seasoned investors swear by SIPs for long-term goals. The dual engines of consistency (SIP) and opportunity capture (RCA) allow gains to spiral via compounding—especially when investors resist the urge to stop during downturns.

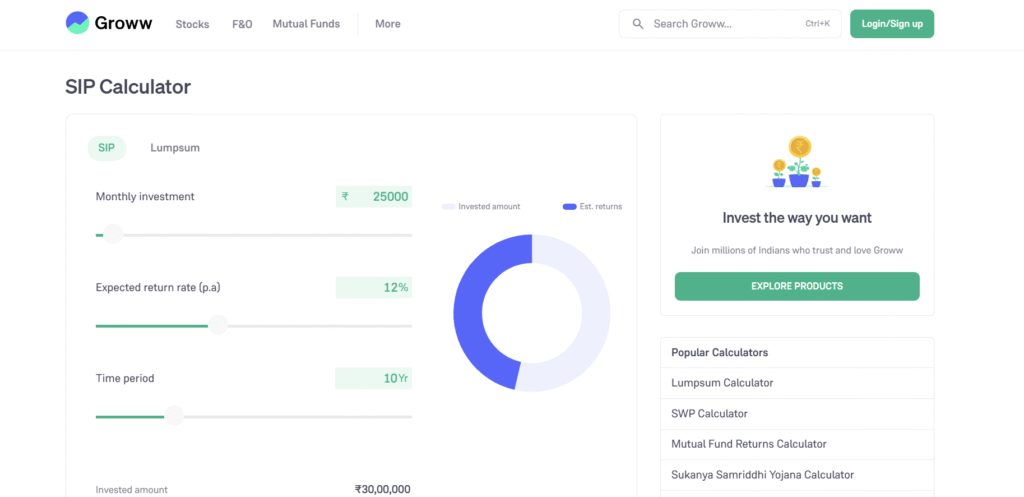

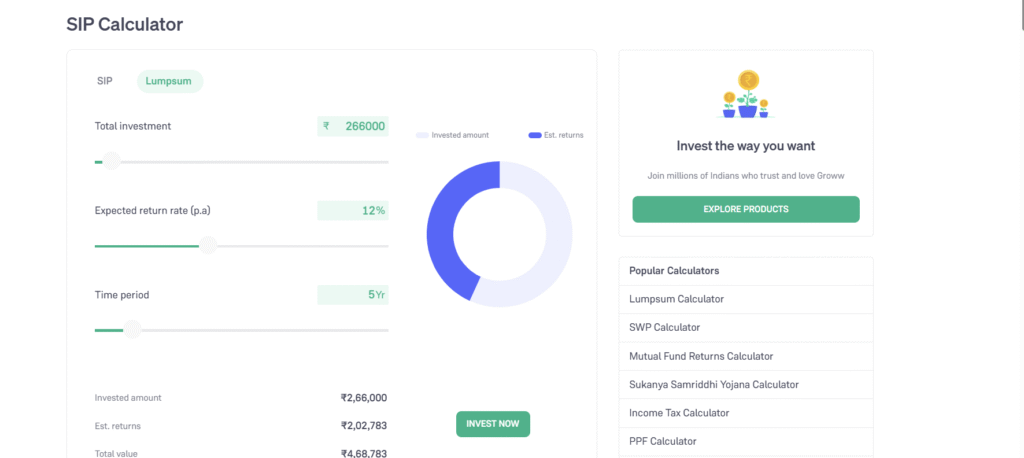

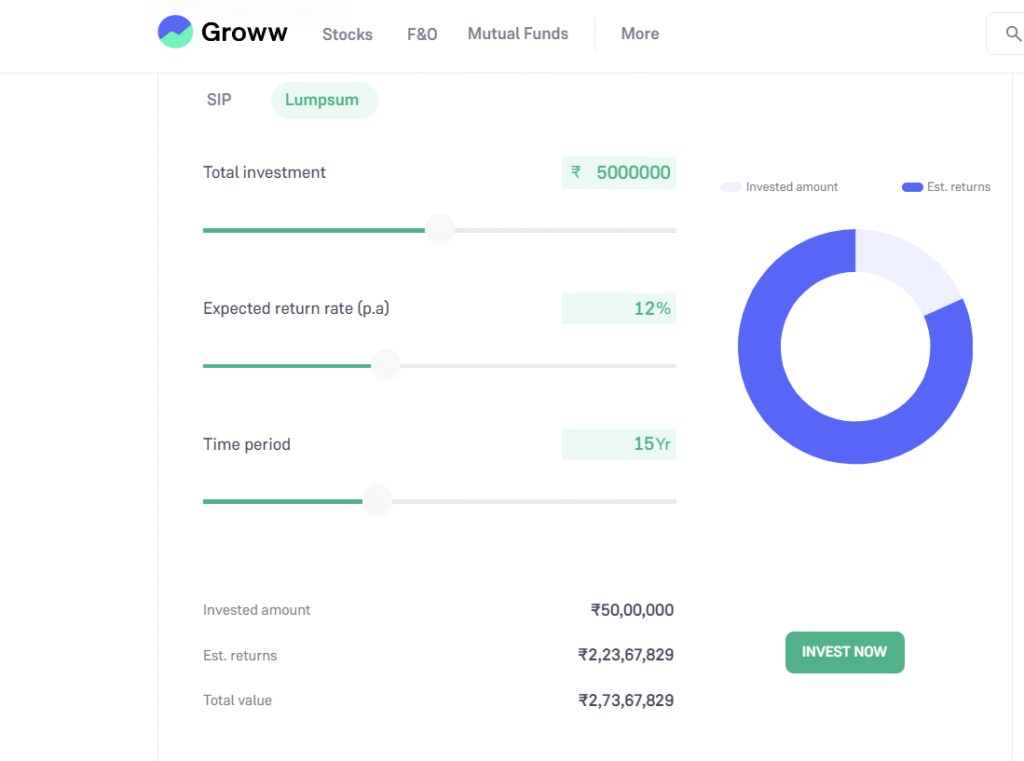

- Case study: Investing ₹10k/month for 15 years at 12% annual return produces over ₹50 lakhs, per Groww’s calculator and verified AMFI data.

- MoneyControl analysis: SIP in Franklin India Prima Plus from 2000–2015 (₹1.8 lakhs total) grew to ₹1.28 crore—not a backtested “ideal,” but real performance numbers.

- Compounding works best late—over half the wealth in a 20-year SIP is generated in the final 5 years.

As one user, u/investingmatters, summarized: “Biggest lesson? Sticking with SIP through thick and thin. Those ‘bad months’ looking back now just got me more units for cheap.”

4. Setting Up a SIP Investment Plan

Step-by-step setup guide

- Define your goal (e.g., “₹50 lakhs in 15 years for child education”).

- Assess your risk tolerance (aggressive, moderate, conservative).

- Pick a suitable mutual fund type (equity for 10+ years, hybrid for 5–10, debt for under 5).

- Shortlist funds: Look at 5-year returns, fund manager stability, and expense ratios.

- Choose “Direct” plans for lowest cost; pick a trusted investment platform/app (Groww, Zerodha, or AMC sites).

- Set up auto-debit/mandate so investments happen without fail.

My first SIP was a modest ₹2,000/month. As my income grew, I increased it yearly. Automated debits removed the temptation to “wait for better timing.”

- Popular apps provide helpful tracking and calculators, making adjustments painless.

- Document your progress—seeing growth can be a huge motivator during rough patches.

5. Calculating Returns with Rupee Cost Averaging

Understanding the math behind SIP returns helps set expectations and optimize plans.

- Formula: M = P × ({[1 + i]^n – 1} / i) × (1 + i) where M = maturity amount, P = monthly investment, i = monthly rate, n = total months.

- Example: ₹5,000/month, 12% annual (0.95% monthly), 10 years yields ~₹11.5 lakhs on ₹6 lakhs invested.

Rupee cost averaging reduces the uncertainty—your average cost per unit ends up significantly lower than peak prices. Groww and MoneyControl both offer reliable SIP calculators to project potential returns.

| Year | Wealth Accumulation (₹5k/month @ 12%) |

|---|---|

| 5 Years | ~₹4.1 lakhs |

| 10 Years | ~₹11.5 lakhs |

| 15 Years | ~₹25 lakhs |

| 20 Years | ~₹47 lakhs |

6. Common Mistakes to Avoid in SIP Investments

- Skipping homework—choosing funds on hype, not proven performance or fit.

- Stopping SIPs during downturns—which destroys the biggest RCA advantage (quote: “The only SIPs I regret are the ones I paused in 2020. Lost my best buying opportunity.” – u/quantswe).

- Misjudging your risk appetite—leading to panic selling or premature withdrawals.

- Chasing fads or sector funds without understanding volatility.

- Ignoring increases—never upping SIP as salary grows, missing compounding power.

In my experience, documenting my reason for each SIP (e.g., “retirement corpus,” “daughter’s degree fund”) stopped me from making emotional decisions.

7. Tips for Maximizing SIP Investments

- Review SIPs annually—keep, remove, or rebalance based on long-term consistency, not short-term returns.

- Step up your SIP contribution yearly (5–10%) with increments/bonuses to supercharge wealth.

- Use direct plans to lower expense ratios over decades.

- Seek independent financial advice if unsure—many online calculators and planners are free.

- Diversify: core diversified equity fund + possible satellite funds (midcap, gold, hybrid).

Redditor u/stepupwise: “Top-up SIPs were a gamechanger. Every annual increment—half to SIP. Result: portfolio grew way faster than just fixed amounts.”

8. The Role of Patience and Discipline in Wealth Creation

Let me be direct: SIPs work only if you stay the course, even when markets nosedive. Those “uncomfortable” months are when you accumulate units at fire-sale prices—and when the market recovers, the jump is dramatic.

- A 2021 Motilal Oswal study tracked investors who continued SIPs during 2008 and 2020 crashes—those who paused returned 7–9%, while disciplined investors achieved 11–13% CAGR.

- It’s normal to feel nervous (I did, too), but sticking with your plan pays off, as so many successful case studies confirm.

- As u/oldschoolinvest put it: “Your patience IS your alpha. Markets will test you—that’s when SIP silently sets you up for future gains.”

Beyond-common-sense insights about SIP and Rupee Cost Averaging

- SIPs turn market volatility from a risk into an advantage: The worse the dip, the more units you acquire, accelerating wealth-building on the rebound.

- Entry timing is overrated: Many investors who started SIPs at the 2008–09 or 2020 peaks still saw stellar returns over 10–15 years—consistency triumphed over luck.

- Incremental SIPs outperform static ones: Top-up (step-up) strategies harness income growth and swiftly magnify results, as confirmed by major AMCs and forum user journeys.

- Each SIP installment is taxed as a unique purchase: Redeeming units after one year optimizes LTCG benefits—each monthly buy starts its own timer for taxation.

- Expense ratios compound against you: A mere 0.5% difference (direct vs regular plan) can erase lakhs in final value for 20-year SIPs, as calculators and case studies reveal.

Conclusion

Reflecting on my own SIP journey, I’m convinced there’s no more accessible or powerful way for regular people to build substantial wealth in India than by pairing systematic investment with rupee cost averaging. Each time I set up a new goal-based SIP—writing down my target, picking a fund fit for my timeline, and automating contributions—I know I’m putting the math and psychology in my favor.

Here’s the recap to get you started (and keep you moving):

- Define your financial goal and timeline as clearly as possible.

- Honestly assess your risk appetite—equity for long, hybrid/debt for short-medium.

- Shortlist funds: favor long-term performance, low costs, and guaranteed diversification.

- Select “Direct” plans through trusted platforms or directly via fund houses.

- Set up bank mandates/auto-debit to stick to your plan.

- Review SIPs once or twice yearly, rebalancing only when needed—not in panic.

- Increase SIP whenever possible (annual increments, bonuses).

- Trust the process: ride out volatility, avoid knee-jerk reactions, and keep perspective on long-term progress—not today’s noise.

Ready to kickstart (or boost) your wealth journey? Share your SIP plans, doubts, or success stories in the comments. Let’s make investing a tool for freedom, not fear—one disciplined step at a time.